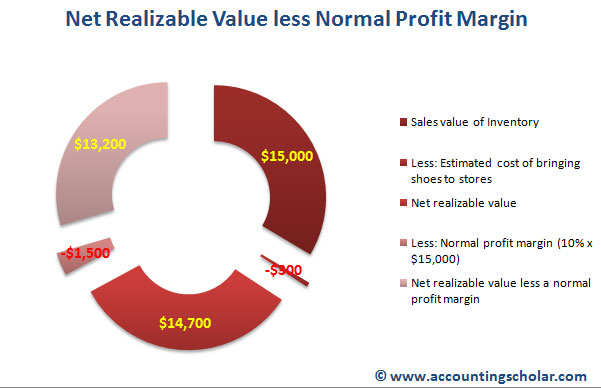

So under the old rule of LCM, replacement cost (what our wholesale distributor sells to them to us for) would be the ceiling. Let’s also say we would normally mark them up and expect to make about $20 on the sale, so the floor, the lowest we could adjust them to, would be $30. If we lowered the cost to $30 on our books and sold them for $70 minus the $20 it takes to make them saleable, we’d make a normal profit. 2The as a dependent independent auditors also analyze the available evidence and must believe that it is sufficient to provide the same reasonable assurance in order to render an unqualified opinion on the financial statements. If the net realizable value calculation results in a loss, then charge the loss to the cost of goods sold expense with a debit, and credit the inventory account to reduce the value of the inventory account.

Controller’s Guide to a Stress-Free Month-End Close

In some cases, NRV of an item of inventory, which has been written down in one period, may subsequently increase. In such circumstances, IAS 2 requires the increase in value (i.e. the reversal), capped at the original cost, to be recognized. Reversals of writedowns are recognized in profit or loss in the period in which the reversal occurs.

Example of NRV Calculation

The net realizable value is defined as the estimated selling price in the ordinary course of business less the estimated costs necessary to make the sale and estimated costs to get the inventory in condition for sale. Other times NRV is used by accountants to make sure an asset’s value isn’t overstated on the balance sheet. If you’re a CPA, you’ll come across NRV within cost accounting, inventory, and accounts receivable. According to the notion of lesser cost or net realizable value, inventory should be recorded at the lower of its cost or the price at which it can be sold. The estimated selling price of something in the regular course of business, less the completion, selling, and shipping costs, is known as the net realizable value. It is accepted in both the accounting standards, GAAP and IFRS to ensure the ending inventory value is neither overestimated nor underestimated.

NRV Video Explanation

- This net amount represents the amount of cash that management expects to realize once it collects all outstanding accounts receivable.

- In other words, market was the price at which you could currently buy it from your suppliers.

- The accounting for the costs of transporting and distributing goods to customers depends on whether these activities represent a separate performance obligation from the sale of the goods.

- In addition, the loss should be recognized as an expense on the income statement.

- For example, if accounts receivable is $50,000 and the allowance for doubtful accounts is $5,000, the cash realizable value is $45,000.

Consequently, officials for Dell Inc. analyzed the company’s accounts receivable as of January 30, 2009, and determined that $4.731 billion was the best guess as to the cash that would be collected. The actual total of receivables was higher than that figure but an estimated amount of doubtful accounts had been subtracted in recognition that a portion of these debts could never be collected. Net Realizable Value (NRV) is the estimated selling price of an asset in the ordinary course of business, minus the estimated costs of completion and the estimated costs necessary to make the sale. Essentially, it’s what a company expects to earn from an asset after accounting for any expenses needed to prepare and sell it. GAAP rules previously required accountants to use the lower of cost or market (LCM) method to value inventory on the balance sheet.

Net Realizable Value Formula

The assessment of net realizable value under IFRS is typically done either item by item or by groups of similar or related items. If the value of inventory declines below the carrying amount on the balance sheet, the inventory carrying amount must be written down to its net realizable value. In addition, the loss should be recognized as an expense on the income statement. This expense can be included as part of the cost of sales or reported separately.

Unlike IAS 2, US GAAP does not contain specific guidance on storage and holding costs, which may give rise to differences from IFRS Standards in practice. Unlike IAS 2, US GAAP allows use of different cost formulas for inventory, despite having similar nature and use to the company. Therefore, each company in a group can categorize its inventory and use the cost formula best suited to it.

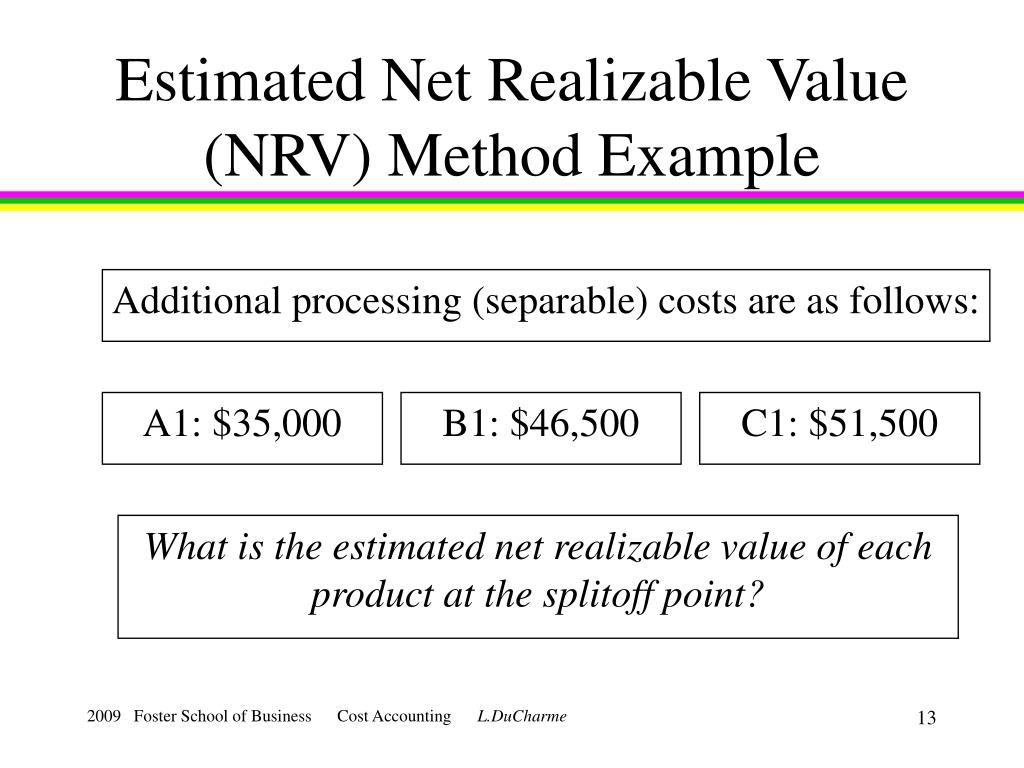

This allows managers to calculate the total cost and assign a sale price to each product individually. It also allows managers to better plan and understand whether to stop production at the split-off point or if it is more advantageous to continue processing the raw material. Understanding NRV and its application not only ensures compliance with accounting standards but also supports effective financial management and strategic planning. For anyone involved in accounting or finance, grasping the concept of NRV is essential for accurate asset valuation and financial analysis.

It has a wooden table in its inventory, and the expected selling price is $1,000. To sell this table, the company needs to spend $50 on finishing touches, $100 on packaging, and $50 on shipping. Consequently, net realizable value is also known as cash realisable value. The terms “net realizable value” and “current assets” are frequently used concerning inventory and accounts receivable. Accounting conservatism is a principle that requires company accounts to be prepared with caution and high degrees of verification. These bookkeeping guidelines must be followed before a company can make a legal claim to any profit.

Dual preparers should carefully assess all differences to prepare a model that is efficient to maintain, most representative of their inventory values and compliant with all applicable requirements under both GAAPs. While both IAS 2 and ASC 330 share similar objectives, certain differences exist in the measurement and disclosure requirements that can affect comparability. Here we summarize what we see as the top 10 differences in measurement of inventories under IFRS Standards and US GAAP. Commercial samples, returnable packaging or equipment spare parts typically do not meet the definition of inventories, although these might be managed using the inventory system for practical reasons. Helping clients meet their business challenges begins with an in-depth understanding of the industries in which they work.

But for calculating the Net Realizable Value, IBM will have to identify the customers who can default on their payments. This amount is entered into accounts as “Provision for Doubtful Debts.” Let’s say this amount is $1 Bn. Are you a business owner looking to complete the eventual sale of equipment or inventory? Net realizable value affects the cost of goods sold (COGS) by determining the lower value between the cost and NRV for inventory. If NRV is lower than the cost, the inventory is written down to NRV, increasing COGS and reducing gross profit.

It is a conservative method, which means that the accountant should post the transaction that does not overstate the value of assets and potentially generates less profit for valuing assets. It usually requires certified public accountants (CPAs) to do the job as it involves a lot of judgment. NRV is also used to account for costs when two products are produced together in a joint costing system until the products reach a split-off point. Each product is then produced separately after the split-off point, and NRV is used to allocate previous joint costs to each of the products. The ultimate goal of NRV is to recognize how much proceeds from the sale of inventory or receipt of accounts receivable will actually be received. This relates to the creditworthiness of the clients a business chooses to engage in business with.