No matter which method you use to find the NRV, the value you find must fit the conservative method of accounting reporting. Our solution has the ability to prepare and post journal entries, which will be automatically posted into the ERP, automating 70% of your account reconciliation 2019 volunteer mileage rates and irs reimbursement guidelines process. Understanding the NRV is essential for businesses to maintain accurate financial records and make informed decisions. In the next section, we will delve into the formula and calculation of NRV, providing a step-by-step guide to ensure clarity and accuracy.

Decommissioning and restoration costs form part of inventory costs under IAS 2; not under US GAAP

GAAP requires that certified public accountants (CPAs) apply the principle of conservatism to their accounting work. Many business transactions allow for judgment or discretion when choosing an accounting method. The principle of conservatism requires accountants to choose the more conservative approach to all transactions. This means that the accountant should use the accounting method that does not overstate the value of assets. Unlike IAS 2, US GAAP does not allow asset retirement obligation costs incurred as a consequence of the production of inventory in a particular period to be a part of the cost of inventory.

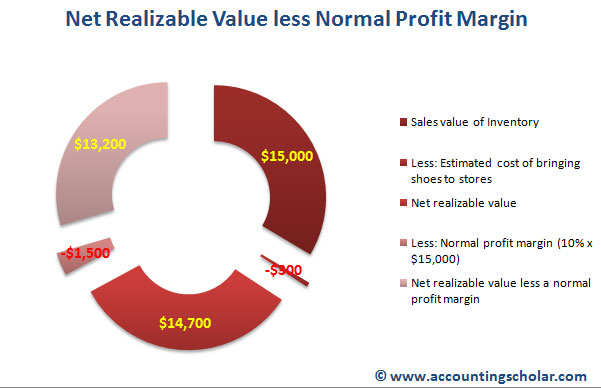

- Thus, the use of net realizable value is a way to enforce the conservative recordation of inventory asset values.

- The subsequent depreciation of the cost is included in production overheads in future periods over the asset’s estimated remaining useful life.

- This amount is entered into accounts as “Provision for Doubtful Debts.” Let’s say this amount is $1 Bn.

- A positive NRV implies that your inventory will generate profits for you, whereas a negative NRV shows that the value of your goods is lower than their cost.

IAS 2 generally measures inventories at the lower of cost and NRV; US GAAP does not

Carrying costs and transactional costs of goods are taken into account to not overstate the income statement, and accurately represent the goods’ value to the business. As technology evolves and production capabilities expand, unsold inventory items may quickly lose their luster and become obsolete. This is true for even recently manufactured products; companies not in tune with market conditions may be producing goods that are already outdated.

Lower of cost or market (LCM) rule

Cash realizable value is calculated by estimating the amount expected to be collected from accounts receivable. Subtract the allowance for doubtful accounts from the total accounts receivable. For example, if accounts receivable is $50,000 and the allowance for doubtful accounts is $5,000, the cash realizable value is $45,000. Incorporating AI into NRV calculations not only makes the process more efficient but also enhances the overall accuracy and reliability of financial reporting. By embracing technological advancements, businesses can stay ahead in an ever-evolving market and ensure their financial practices are robust and forward-thinking.

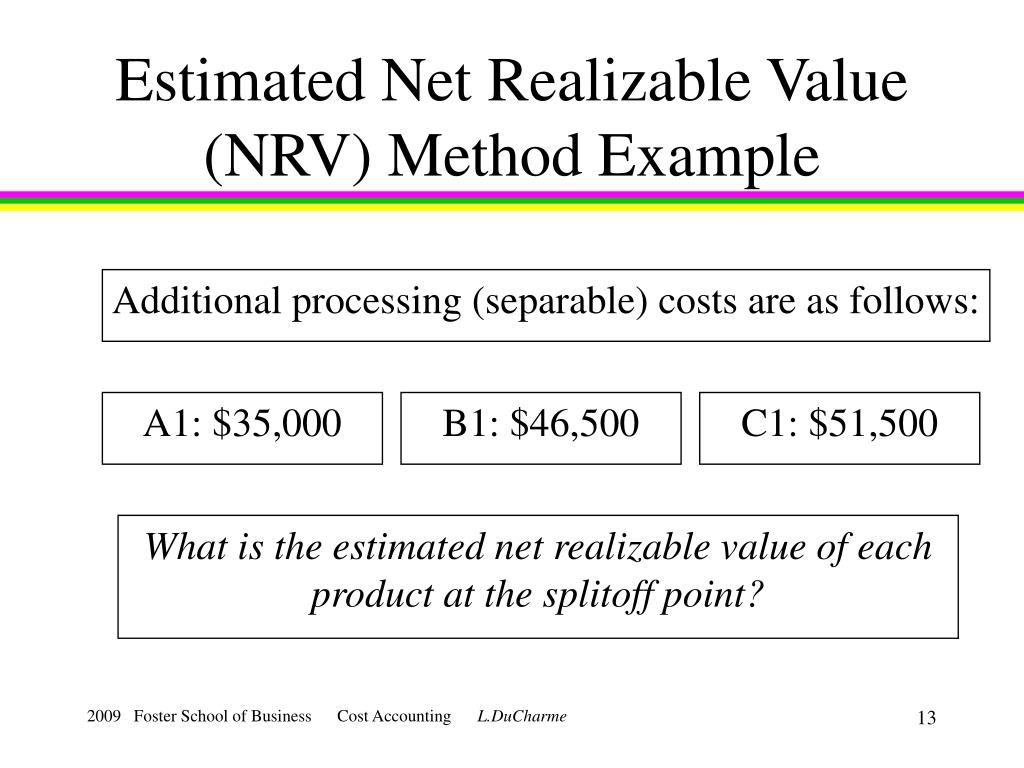

Net Realizable Value of an asset is at which it can be sold after deducting the cost of selling or disposing of the asset. Since in NRV, a firm also considers the cost, hence it is known as a conservative approach to the transaction. Net realizable value can also refer to the aggregate total of the ending balances in the trade accounts receivable account and the offsetting allowance for doubtful accounts. This net amount represents the amount of cash that management expects to realize once it collects all outstanding accounts receivable. The calculation for Net Realizable Value has a variety of methods to get an answer.

There are different methods for calculating this depending on the purpose of finding the NRV. Mostly like you won’t have to break out the calculator since the formula is very simple. Calculating the net realizable value involves a straightforward process that ensures assets are valued correctly. A positive NRV implies that your inventory will generate profits for you, whereas a negative NRV shows that the value of your goods is lower than their cost. Loosely related to obsolescence, market demand refers to customer preferences, tastes, and other influencing factors.

Unlike US GAAP, inventories are generally measured at the lower of cost and NRV3 under IAS 2, regardless of the costing technique or cost formula used. Say Geyer Co. bought 200 Rel 5 HQ Speakers five years ago for $110 each and sold 90 right off the bat, but has only sold 10 more in the past two years for $70. There are still a hundred on hand, costs using FIFO, but the speakers are obsolete and management feels they can sell them with some slight modifications to each one that cost $20 each. US GAAP, although broadly consistent with IFRS, prohibits the reversal of write-downs.

Techniques for measuring the cost of inventories, such as the standard cost method or the retail method, may be used for convenience if the results approximate cost. HighRadius offers a cloud-based Record to Report Suite that helps accounting professionals streamline and automate the financial close process for businesses. We have helped accounting teams from around the globe with month-end closing, reconciliations, journal entry management, intercompany accounting, and financial reporting. This helps businesses determine the net amount they can expect to receive from selling an asset after accounting for any additional costs involved in the sale.