Non-manufacturing costs – not incurred in transforming materials to finished goods. These include selling expenses (such as advertising costs, delivery expense, salaries and commission of salesmen) and administrative expenses (such as salaries of executives and legal expenses). Manufacturing costs – incurred in the factory to convert raw materials into finished goods.

- Steel and plastics have the highest overall contribution due to the very large demand for these materials.

- A balance sheet is one of the financial statements that gives a view of the company’s financial position, while assets are the resources a company owns.

- As a result, the company decided to outsource production to a contract manufacturing company (a company that enters into a contract with the manufacturer to make certain components) instead of assembling components in-house.

- Each of them requires a different set of cost control measures, making appropriate cost categorization even more essential.

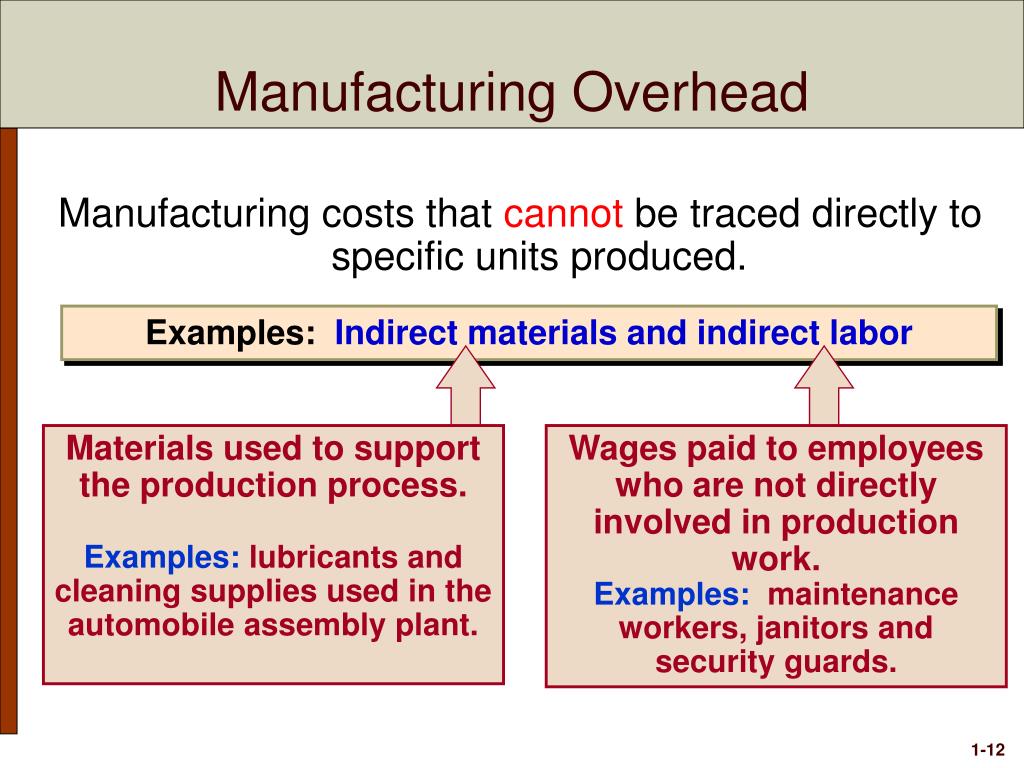

- Direct materials – cost of items that form an integral part of the finished product.

Direct Labor

Standard cost – predetermined cost based on some reasonable basis such as past experiences, budgeted amounts, industry standards, etc. Fixed costs – costs that remain constant regardless of the level of activity. Examples include rent, insurance, and depreciation using the straight line method. Direct materials are raw materials that become an integral part of the finished goods.

Financial Reporting vs. Individual Products and Customers

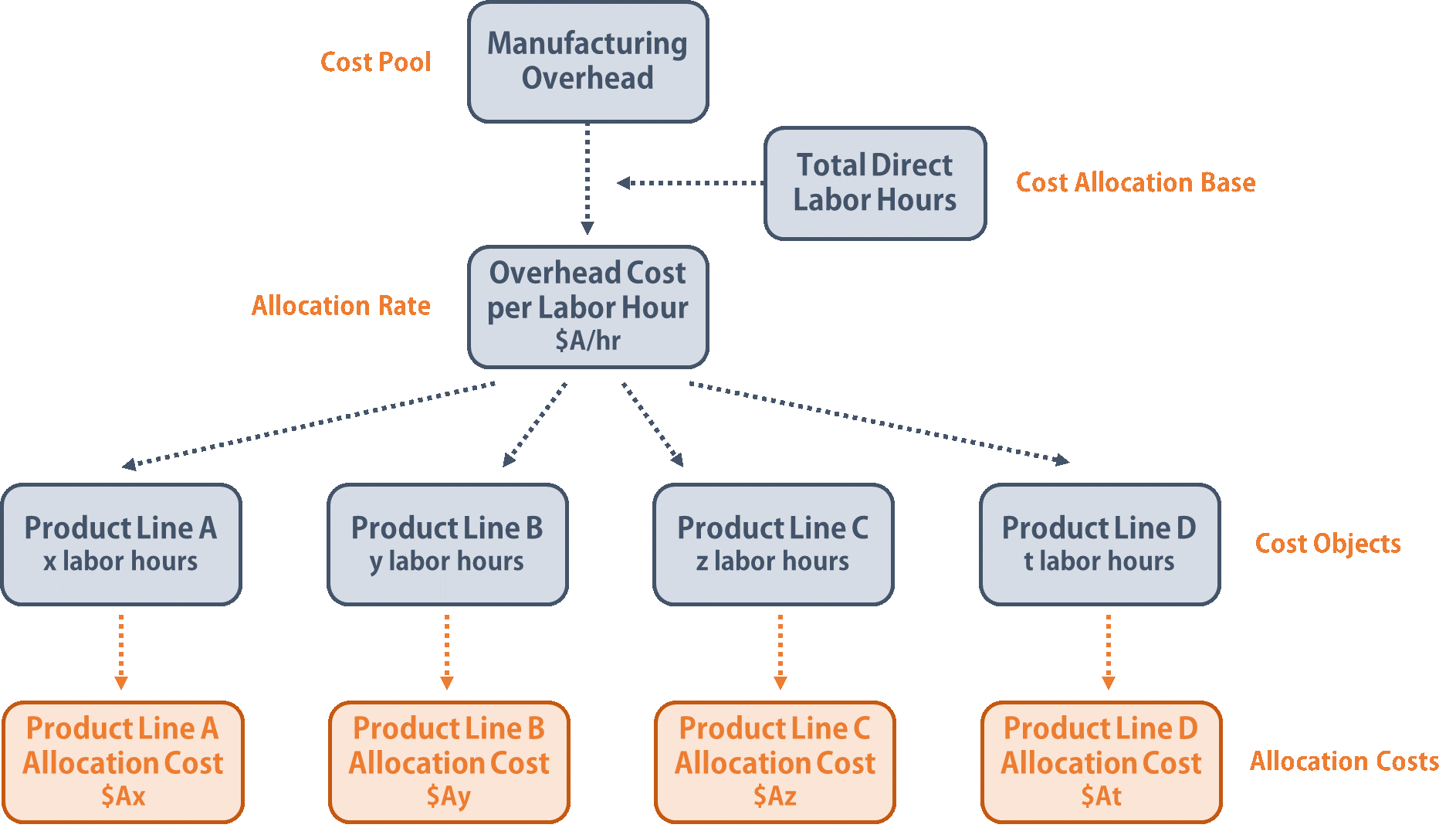

With all this valuable information under your belt, you can better track manufacturing costs as they pertain to your workforce. Here are some frequently asked questions (FAQs) and answers that address key concepts related to manufacturing costs. With a breakup of all the costs of manufacturing, management can decide whether it is more profitable to purchase certain parts or materials from a vendor or manufacture them in-house. As you can see, by collecting cost data and calculating it accurately, businesses can optimize cost management and set the right price for their products to gain a competitive advantage. Here’s an interesting case study on how manufacturing cost analysis helped a steel manufacturing company save costs.

What are direct manufacturing costs?

Manufacturing costs include direct materials, direct labor, and factory overhead. To help clarify which costs are included in these three categories, let’s look at a furniture company that specializes in building custom wood tables called Custom Furniture Company. Each table is unique and built to customer specifications for use in homes (coffee tables and dining room tables) and offices (boardroom and meeting room tables). The sales price of each table varies significantly, from $1,000 to more than $30,000.

Both of these figures are used to evaluate the total expenses of operating a manufacturing business. The revenue that a company generates must exceed the total expense before it achieves profitability. Direct labor would include the workers who use the wood, hardware, glue, lacquer, and other materials to build tables.

Production Costs vs. Manufacturing Costs Example

In the end, management should know whether each product’s selling price is adequate to cover the product’s manufacturing costs, nonmanufacturing costs, and required profit. These costs are not directly tied to the production of goods or services, but rather to the overall operation of the company. Examples of period costs may include rent, salaries and wages of administrative staff, office supplies, marketing and advertising expenses, and other similar expenses. While these costs are necessary for the overall functioning of the business, they do not directly contribute to the production of goods or services.

The next step is to calculate the costs of utilities (electricity, water, or gas) that are directly used in the manufacturing process (for example, fuel used to operate the production equipment). While this is a simplified view of direct turbo tax 2011 for sale labor calculation, accountants also include the benefits, overtime pay, training costs, and payroll taxes when calculating the hourly rate. Mixed costs – costs that vary in total but not in proportion to changes in activity.

Nonmanufacturing overhead costs are the company’s selling, general and administrative (SG&A) expenses plus the company’s interest expense. In this example, the total production costs are $900 per month in fixed expenses plus $10 in variable expenses for each widget produced. To produce each widget, the business must purchase supplies at $10 each. After subtracting the manufacturing cost of $10, each widget makes $90 for the business.

Examples include wood in furniture, steel in automobile, water in bottled drink, fabric in shirt, etc. Just under half of the climate costs – 42% – came from manufacturing processes, rather than energy use. For example, making cement produces carbon dioxide because of the chemical reactions involved, in addition to any energy consumed. Manufacturing costs, for the most part, are sensitive to changes in production volume. Manufacturing businesses calculate their overall expenses in terms of the cost of production per item. That number is, of course, critical to setting the wholesale price of the item.

Some operating expenses can also be classified as direct costs, such as advertising cost for a particular product. Recall from other tutorials that variable costs change in proportion to production. For instance, in our example of Friends Company, the company purchases metal parts (raw material) to produce valves. The more valves are produced, the more parts Friends Company has to acquire. Therefore, parts have a variable nature; the amount of raw materials bought and used changes in direct proportion to the amount of valves created.

The relevance of costing to manufacturing companies is highly important to running an efficient and successful business. Identifying, separating and apportioning cost data provides management and outside decision makers (investors) valuable information on the company’s profitability and cost control systems. While depreciation on manufacturing equipment is considered a manufacturing cost, depreciation on the warehouse in which products are held after they are made is considered a period cost. While carrying raw materials and partially completed products is a manufacturing cost, delivering finished products from the warehouse to clients is a period expense.