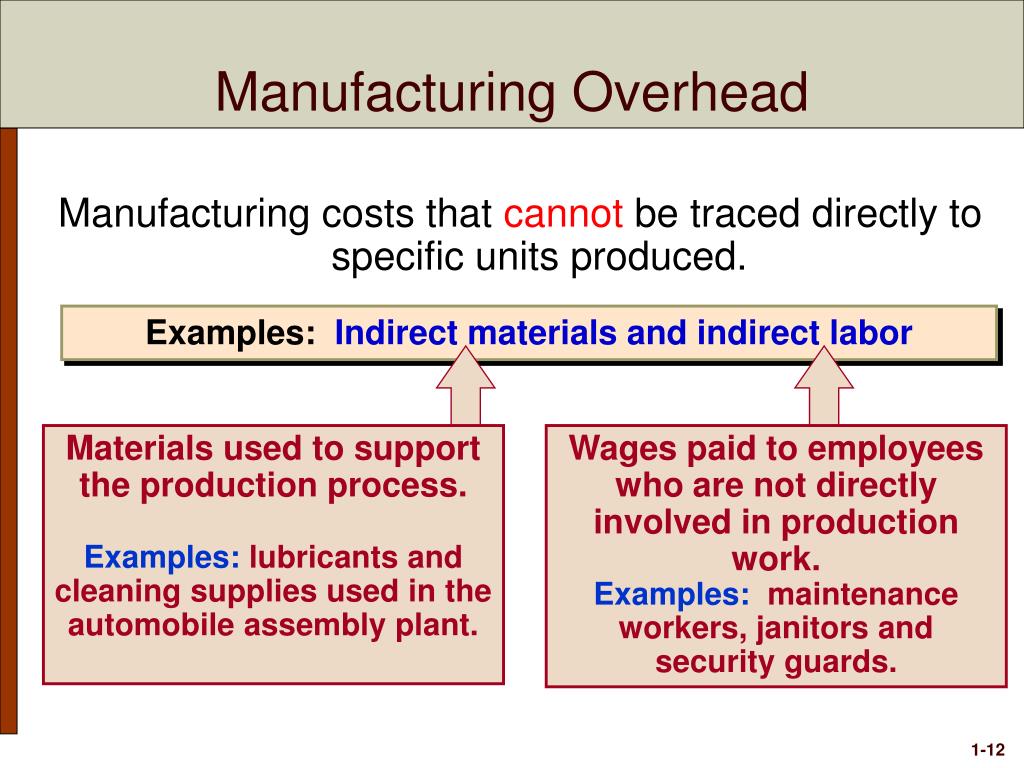

It includes cost of raw materials used (direct materials), direct labor, and factory overhead. On the other hand, a product with a low gross profit may actually be very profitable, if it uses only a minimal amount of administrative and selling expense. Direct labor manufacturing costs is determined by calculating the cost of employees directly responsible for producing the product. For example, a clothing manufacturer considers employees that dye the cloth, cut the cloth and sew the cloth into a garment as direct labor costs. However, designers and sales personnel are considered nonmanufacturing labor costs. Costs that are not related to the production of goods are called nonmanufacturing costs; they are also referred to as period costs.

Strategic Cost Management

Start by making a list of all the direct materials that are used to make the specific product and obtain the cost information for the direct materials you have identified. To calculate the cost of direct materials you need to know the cost of inventory. According to McKinsey’s research, cutting down manufacturing costs, in addition to boosting productivity, is the key for manufacturing companies to remain competitive.

Differences between management and tax accounting

Direct labor – cost of labor expended directly upon the materials to transform them into finished goods. Direct labor refers to salaries and wages of employees who work to convert the raw materials to finished goods. Incorporating climate costs shows that the real cost of manufacturing these materials is much higher than current market prices. Adopting policies that reflect these costs can create incentives to develop new, climate-friendly processes and materials. Note “Business in Action 2.3.1” details the materials, labor, and manufacturing overhead at a company that has been producing boats since 1968. For example, a small business that manufactures widgets may have fixed monthly costs of $800 for its building and $100 for equipment maintenance.

General and Administrative Costs

These costs have two components—selling costs and general and administrative costs—which are described next. Costs that are not related to the production of goods are called nonmanufacturing costs23; they are also referred to as period costs24. Non-manufacturing costs refer to expenses that are not directly tied to the production of goods or services. These costs encompass a variety of expenses such as selling, administrative, and research and development costs, which support the overall operations of a business but do not contribute to the creation of products. Understanding non-manufacturing costs is essential for effective budgeting and financial planning as they impact overall profitability and can influence pricing strategies. Manufacturing costs refer to those that are spent to transform materials into finished goods.

Manufacturers can compare the costs of making a product using different manufacturing processes. This helps them understand the most efficient process and the investment they need to make for the selected process. A manufacturing company initially purchased individual components from different vendors and assembled them in-house. As the company decided to assemble the components themselves, they found that the costs of managing the assembly line and the transportation were increasing significantly.

Step #3: Add up the other direct expenses

The manufacturing dataset will inform both practical and policy work, Kane said. The same methods could also be replicated for other sectors of the economy. Steel and plastics have the highest overall contribution due to the very large demand for these materials.

As the manufacturing process involves raw materials and finished goods, all of these are considered assets. The materials that are yet to be assembled /processed and sold are considered work-in-process or work-in-progress (WIP) inventory. Another commonly used term for manufacturing costs is product costs, which also refer to the costs of manufacturing a product.

- Tracking the number of hours each employee works on the production line can be tricky.

- Combining her knowledge of multiple disciplines, she seeks to help others optimize their work-life balance, which she believes is the key to minimizing stress.

- That number is, of course, critical to setting the wholesale price of the item.

- Direct labor would include the workers who use the wood, hardware, glue, lacquer, and other materials to build tables.

- This is an estimate of the costs of carbon dioxide emissions, such as preventing, mitigating and recovering from climate-related natural disasters.

For Friends Company, other direct materials would include, for example, plastic parts and paint. Sometimes it is difficult to discern between manufacturing and non-manufacturing costs. For instance, are the salaries of accountants who manage factory payrolls considered manufacturing or non-manufacturing expenses?

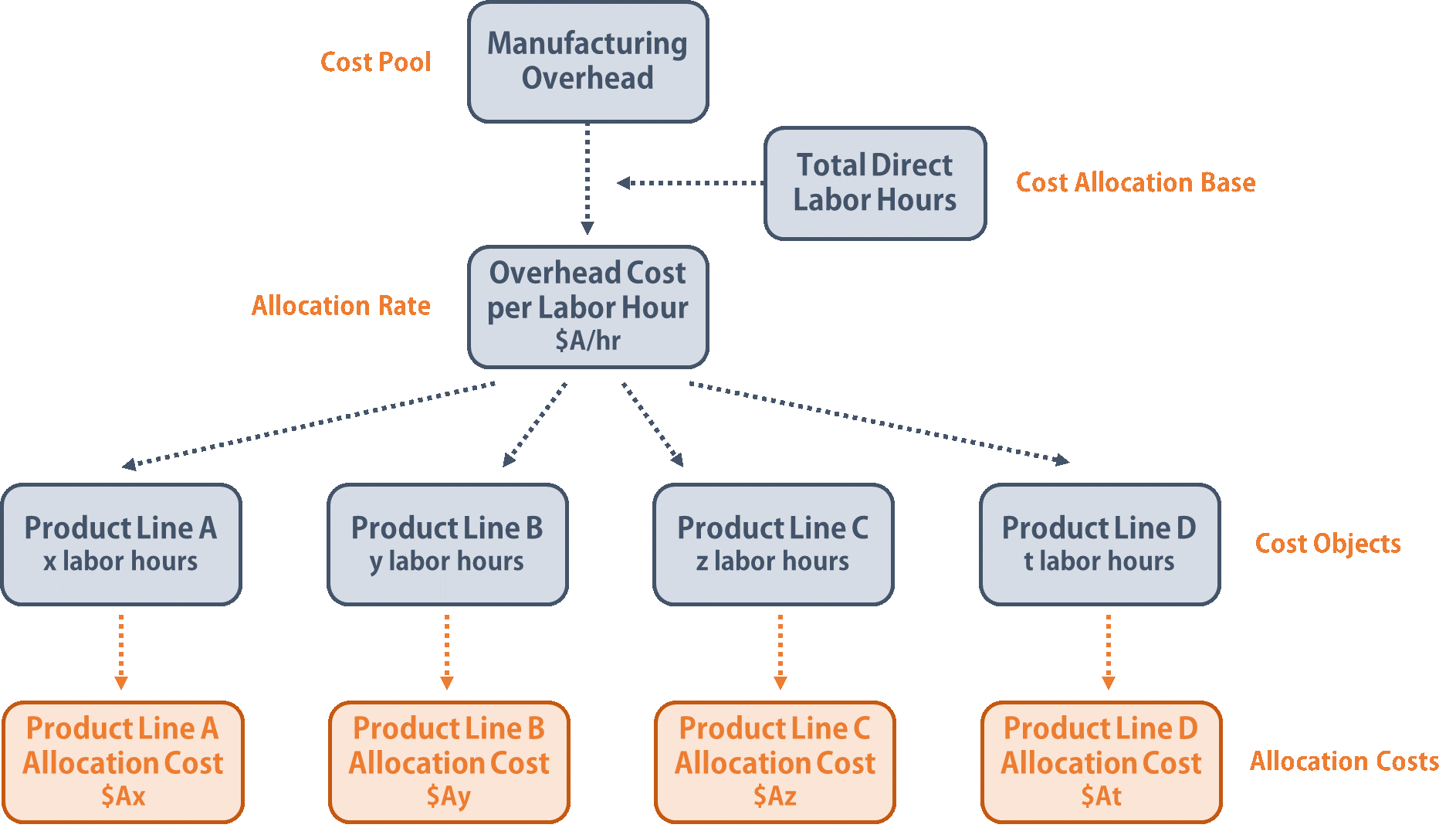

For example, you can allocate depreciation costs of refrigerators to the department that uses them. As employees use Clockify to clock in and out, employers gain insights into the total number of instructions 2021 hours each employee worked on each production line. You can also see the total number of hours worked by the entire team. The company purchases $1,000 worth of new materials to make product X.

For instance, if some raw materials are driving up costs, manufacturers can negotiate with other suppliers who may be willing to supply these materials at a lower cost. According to the book Manufacturing Cost Estimating, the benefits of calculating the costs of manufacturing range from guiding investment decisions to cost control. Fabrizi also talked about the common challenges manufacturers face when calculating the costs of production. In his experience, the most common challenges are a lack of accurate data and the complexity of costing methods. Tracking the number of hours each employee works on the production line can be tricky. This is where a manufacturing time tracking app, such as Clockify, comes in handy.

After manufacturing product X, let’s say the company’s ending inventory (inventory left over) is $500. Therefore, always consult with accounting and tax professionals for assistance with your specific circumstances. Manufacturing costs are also known as factory costs or production costs. Accounting for these costs in market prices could encourage progress toward climate-friendly alternatives. For instance, let’s say the hourly rate a manufacturing company pays to its employees is $30.