The cash flow statement also encourages management to focus on generating cash. They can be calculated using the beginning and ending balances of various asset and liability accounts and assessing their net decrease or increase. This section covers cash transactions from all of a business’ operational activities, such as receipts from sales of goods and services, wage payments to employees, payments to suppliers, interest payments, and tax payments. Companies must be able to generate sufficient positive cash flow for operational growth.

What is an IOLTA Account & 5 Mistakes to Avoid

Whether you’re a working professional, business owner, entrepreneur, or investor, knowing how to read and understand a cash flow statement can enable you to extract important data about the financial health of a company. Purchase of Equipment is recorded as a new $5,000 asset on our income statement. It’s an asset, not cash—so, with ($5,000) on the cash flow statement, we deduct $5,000 from cash on hand. Meaning, even though our business earned $60,000 in October (as reported on our income statement), we only actually received $40,000 in cash from operating activities. So, even if you see income reported on your income statement, you may not have the cash from that income on hand.

How confident are you in your long term financial plan?

Bench simplifies your small business accounting by combining intuitive software that automates the busywork with real, professional human support. Additionally, it shows where we find the calculated or referenced data to fill in the forecast period section. When all three statements are built in Excel, we now have what we call a “Three-Statement Model”.

Cash Flow Statement: Explanation and Example

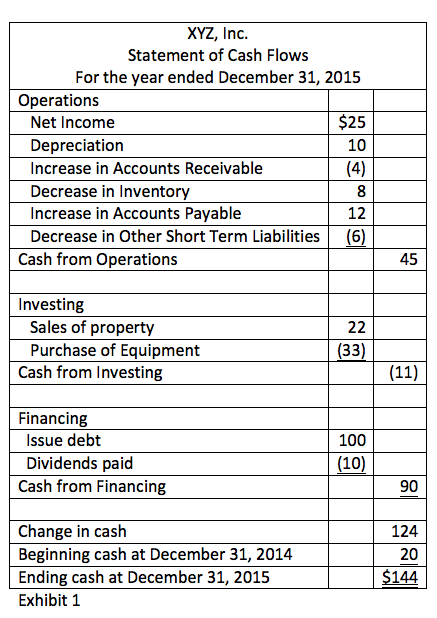

The operating activities section of the statement of cash flows begins with net income. All lines thereafter, in that section, are then adjustments to reconcile net income to actual cash flows by adding back noncash expenses like depreciation and adjusting for changes in asset and liability accounts. The third section of the cash flow statement lists the information for the company’s financing activities. Financing activities include purchases of bonds and stock as well as dividend payments. Some of the applicable ledger accounts include your capital equipment and paid-in capital accounts, notes and bonds payable, stock and retained earnings.

Is the Indirect Method of the Cash Flow Statement Better Than the Direct Method?

Generally, cash flow is reduced when capital expenditures increase, as the cash has been used to invest in future operations, thus promoting the company’s growth. We explain cash flow classification issues and noncash disclosure requirements in detail, with special how to file taxes with irs form 1099 attention to recent SEC statements. We provide new and updated interpretive guidance on applying ASC 230 to many areas, including crypto assets, insurance contracts, debt securities, employee share purchase plans (ESPPs) and tax receivable agreements.

The business brought in $53.66 billion through its regular operating activities. Meanwhile, it spent approximately $33.77 billion in investment activities, and a further $16.3 billion in financing activities, for a total cash outflow of $50.1 billion. What makes a cash flow statement different from your balance sheet is that a balance sheet shows the assets and liabilities your business owns (assets) and owes (liabilities). The cash flow statement simply shows the inflows and outflows of cash from your business over a specific period of time, usually a month. As we have discussed, the operating section of the statement of cash flows can be shown using either the direct method or the indirect method. With either method, the investing and financing sections are identical; the only difference is in the operating section.

Companies categorize their cash flows into operating, investing, and financing cash flows. When a statement of cash flows is prepared, these three types of cash flows are reported under separate sections, which are the operating activities section, the investing activities section, and the financing activities section. The cash flow statement shows the source of cash and helps you monitor incoming and outgoing money. Incoming cash for a business comes from operating activities, investing activities and financial activities.

- This section records the cash flow between the company, its shareholders, investors, and creditors.

- Remember that the indirect method begins with a measure of profit, and some companies may have discretion regarding which profit metric to use.

- Also, when using the indirect method, you do not have to go back and reconcile your statements with the direct method.

- This is a good sign as it tells that the company is able to pay off its debts and obligations.

However, the cash flow statement also has a few limitations, such as its inability to compare similar industries and its lack of focus on profitability. Consequently, the business ended the year with a positive cash flow of $1.5 million and total cash of $9.88 million. This cash flow statement shows that Nike started the year with approximately $8.3 million in cash and equivalents. It can be considered as a cash version of the net income of a company since it starts with the net income or loss, then adds or subtracts from that amount to produce a net cash flow figure. For an investment company or a trading portfolio, equity instruments or receipts for the sale of debt and loans are also included because it is counted as a business activity. Analysts use the CFF section to determine how much money the company has paid out via dividends or share buybacks.

As for the balance sheet, the net cash flow reported on the CFS should equal the net change in the various line items reported on the balance sheet. This excludes cash and cash equivalents and non-cash accounts, such as accumulated depreciation and accumulated amortization. For example, if you calculate cash flow for 2019, make sure you use 2018 and 2019 balance sheets. The direct method adds up all of the cash payments and receipts, including cash paid to suppliers, cash receipts from customers, and cash paid out in salaries. This method of CFS is easier for very small businesses that use the cash basis accounting method. Cash flows from financing (CFF) is the last section of the cash flow statement.

After determining the change in cash, the first step in preparing the statement of cash flows is to calculate the cash flows from operating activities, using either the direct or indirect method. The second step is to analyze all of the noncurrent accounts and additional data for changes resulting from investing and financing activities. The third step is to arrange the information gathered in steps 1 and 2 into the proper format for the statement of cash flows. A cash flow statement is a financial statement that provides aggregate data regarding all cash inflows that a company receives from its ongoing operations and external investment sources. It also includes all cash outflows that pay for business activities and investments during a given period.

Amount of increase (decrease) in noncurrent operating liabilities classified as other. In May 2023 the Board issued Supplier Finance Arrangements (Amendments to IAS 7 and IFRS 7) to require an entity to provide additional disclosures about its supplier finance arrangements. Cash flow from operations are calculated using either the direct or indirect method. PwC refers to the US member firm or one of its subsidiaries or affiliates, and may sometimes refer to the PwC network. This content is for general information purposes only, and should not be used as a substitute for consultation with professional advisors. From the above example, we can see that the computed cash flow for FY 2018 was $ 2,528,000.