By applying NRV calculations, companies can ensure their financial statements reflect a more accurate and realistic financial position. The significance of inventory for certain industries makes accounting and valuation a pertinent focus area. This is because changing inventory costing methodologies often requires systems and process changes. These GAAP differences can also affect the composition of costs of sales and performance measures such as gross margin. In previous chapters, the term “accounts receivable” was introduced to report amounts owed to a company by its customers. GAAP, the figure that is presented on a balance sheet for accounts receivable is its net realizable value—the amount of cash the company estimates will be collected over time from these accounts.

Lower of cost or market (old rule)

- Here we summarize what we see as the top 10 differences in measurement of inventories under IFRS Standards and US GAAP.

- Because of various uncertainties, many of the figures reported in a set of financial statements represent estimations.

- We empower accounting teams to work more efficiently, accurately, and collaboratively, enabling them to add greater value to their organizations’ accounting processes.

- GAAP, the figure that is presented on a balance sheet for accounts receivable is its net realizable value—the amount of cash the company estimates will be collected over time from these accounts.

Thus, the figure reported in the asset section of the balance sheet is lower than the total amount of receivables held by the company. This is the meaning of an accounts receivable balance presented according to U.S. Officials believe they have evidence that any eventual difference with the cash collected will be so small that the same decisions would have been made even if the exact outcome had been known at the time of reporting. The difference between reported and actual figures is most likely to be inconsequential. Once again, though, absolute assurance is not given for such reported balances but merely reasonable assurance.

Presentation of Losses from Net Realizable Value

US GAAP allows the use of any of the three cost formulas referenced above. While the majority of US GAAP companies choose FIFO or weighted average for measuring their inventory, some use LIFO for tax reasons. Companies using LIFO often disclose information using another cost formula; such disclosure reflects the actual flow of goods through inventory for the benefit of investors.

Inventory accounting: IFRS® Standards vs US GAAP

In the following year, the market value of the green widget declines to $115. The cost is still $50, and the cost to prepare it for sale is $20, so the net realizable value is $45 ($115 market value – $50 cost – $20 completion cost). Since the net realizable value of $45 is lower than the cost of $50, ABC should record a loss of $5 on the inventory item, thereby reducing its recorded cost to $45.

Inventories are generally measured at the lower of cost and net realizable value (NRV)3. Cost includes not only the purchase cost but also the conversion and other costs to bring the inventory to its present location and condition. If items of inventory are not interchangeable or comprise goods or services for specific projects, then cost is determined on an individual item basis. Conversely, when there are many interchangeable items, cost formulas – first-in, first-out (FIFO) or weighted-average cost – may be used.

How is IAS 2 different from US GAAP?

In addition to a good becoming outdated, broad markets may be interested in substitute products, advanced products, or cheaper products. Competition always runs the risk of supplanting a good’s market position, even if both goods are still relevant and highly functioning. By submitting, you agree that KPMG LLP may process any personal information you provide pursuant to KPMG LLP’s Privacy Statement.

Entities shall not measure physical inventories at fair value, except as provided by guidance in other Topics. A large company like Home Depot that has a consistent mark-up can reasonably estimate ending inventory. Home Depot undoubtedly uses a more sophisticated version of this calculation, but the basic idea would be the same. If the replacement cost had been $45, we would write the inventory down to $45. If the replacement cost had been $20, the most we could write the inventory down to would be the floor of $30.

Despite similar objectives, IAS 21 differs from ASC 330 in a number of areas2. Here we summarize what we see as the main differences on inventory accounting between the two standards. Net realizable value is the estimated selling price of goods, minus the cost of their sale or disposal. It is used in the determination of the lower of cost or market for on-hand inventory items. The deductions from the estimated selling price are any reasonably predictable costs of completing, transporting, and disposing of inventory.

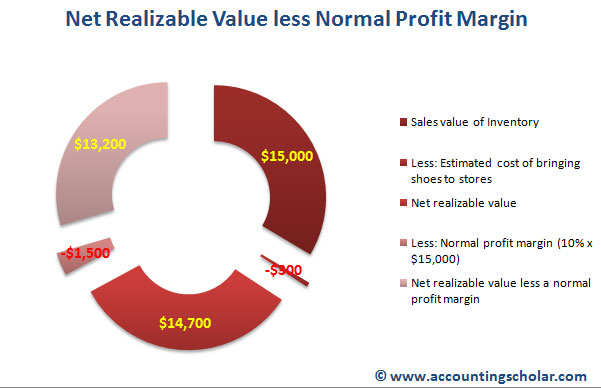

The old rule (that still applies to entities that use LIFO or a retail method of inventory measurement) required entities to measure inventory at the LCM. The term market referred to either replacement cost, net realizable value (commonly called “the ceiling”), or net realizable value (NRV) less an approximately normal profit margin (commonly called “the floor”). Clearly, the reporting of receivables moves the coverage of financial accounting into more complicated territory.

Under GAAP, inventories are measured at lower of cost or market provided that the market value must not exceed the NRV of inventory. Net realizable value is a valuation method used to value assets on a balance sheet. NRV is calculated by subtracting the estimated selling cost from the selling price. NRV is generally used on financial statements for assets that will be sold in the foreseeable future, not the ones expected to go up for liquidation. Net realizable value (NRV) is a method used to determine the actual value of an asset when sold, after deducting any costs involved in the sale.

This ensures that businesses have a realistic view of their financial standing. NRV is particularly important for valuing inventory and accounts receivable. By calculating NRV, businesses can avoid overestimating the value of their assets, which how to calculate and record the bad debt expense enhances financial reporting accuracy and supports better decision-making. Net realizable value (NRV) in accounting is the estimated selling price of an asset in the ordinary course of business, minus any costs to complete and sell the asset.