We use the term nonmanufacturing overhead costs or nonmanufacturing costs to mean the Selling, General & Administrative (SG&A) expenses and Interest Expense. Under generally accepted accounting principles (GAAP), these expenses are not product costs. (Product costs only include direct material, direct labor, and manufacturing overhead.) Nonmanufacturing costs are reported on a company’s income statement as expenses in the accounting period in which they are incurred. Distinguishing between the two categories is critical because the category determines where a cost will appear in the financial statements. As we indicated earlier, nonmanufacturing costs are also called period costs; that is because they are expensed on the income statement in the time period in which they are incurred. Nonmanufacturing costs are necessary to carry on general business operations but are not part of the physical manufacturing process.

Nonmanufacturing overhead costs definition

Then, add up the cost of new inventory — this is the cost of raw materials you purchase to manufacture the product. The opportunity to achieve a lower per-item fixed cost motivates many businesses to continue expanding production up to total capacity. In fact, you already know that labor costs can spiral out of control if you don’t meticulously monitor them. A balance sheet is one of the financial statements that gives a view of the company’s financial position, while assets are the resources a company owns. These assets have value and the company can sell them to earn revenue.

These California climate leaders all have one thing in…

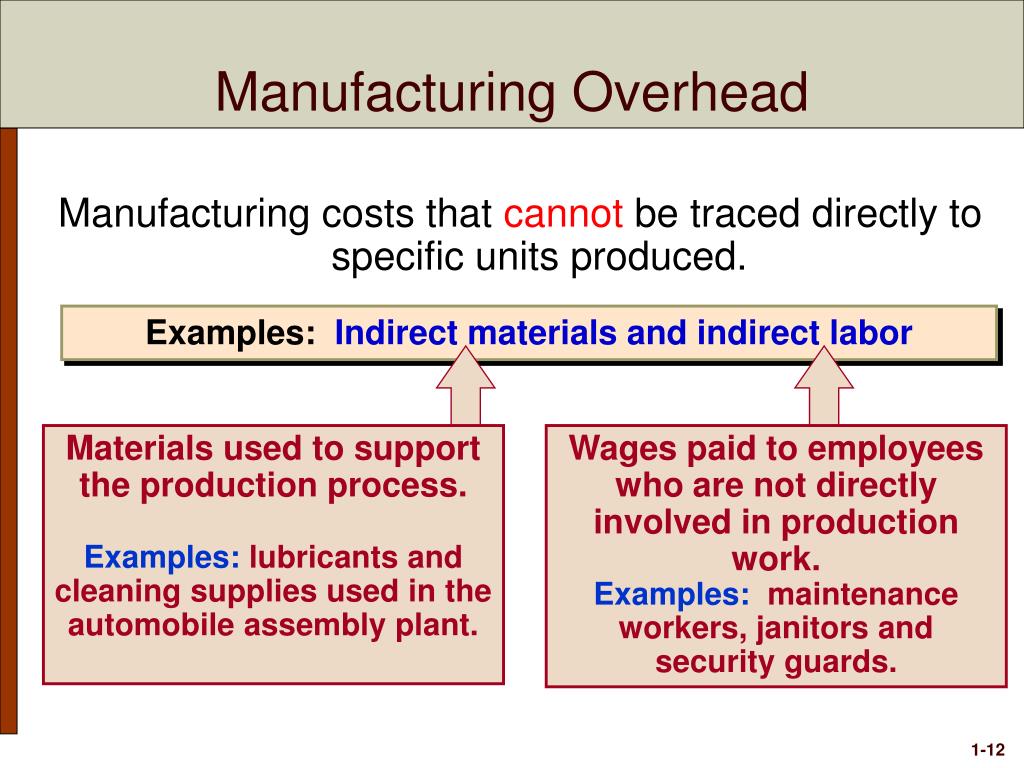

Small, inexpensive items like glue, nails, and masking tape are typically not included in direct materials because the cost of tracing these items to the product outweighs the benefit of having accurate cost data. These minor types of materials, often called supplies or indirect materials, are included in manufacturing overhead, which we define later. Manufacturing costs initially form part of product inventory and are expensed out as cost of goods sold only when the inventory is sold out. Non-manufacturing costs, on the other hand, never get included in inventory rather are expensed out immediately as incurred. This is why the manufacturing costs are often termed as product costs and non-manufacturing costs are often termed as period costs.

Differences between management and tax accounting

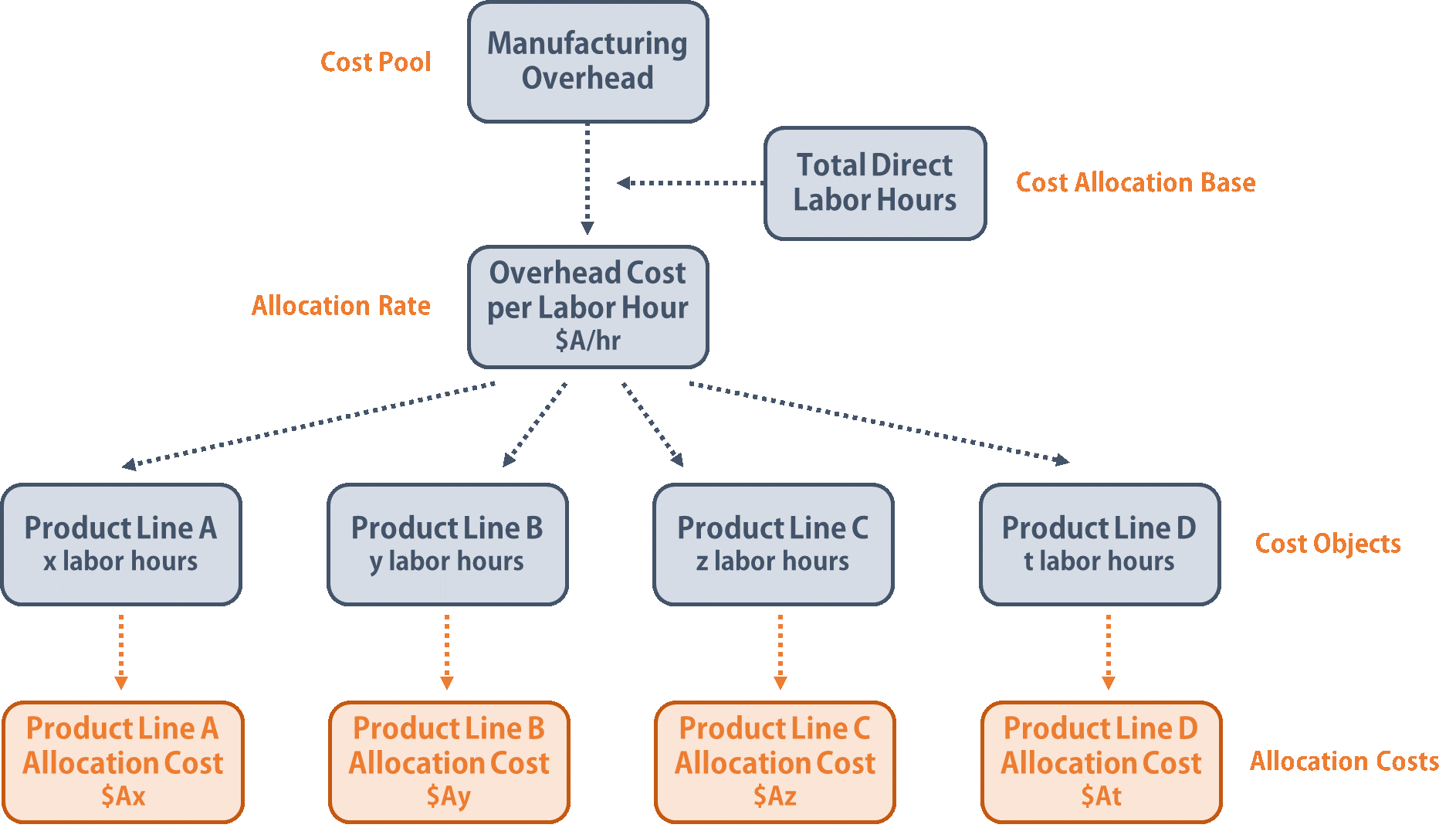

Be sure to allocate overhead costs to the respective cost centers (specific departments, processes, or machines in the manufacturing facility that contribute to the manufacturing costs). Accurate cost calculation helps companies identify the processes or materials that are driving up manufacturing costs and determine the right pricing of products — the keys to remaining profitable. Indirect costs – those that cannot be traced to a particular object of costing. Indirect costs include factory overhead and operating costs that benefit more than one product, department, or branch.

1. Direct materials as a type of manufacturing costs

All manufacturing costs (direct materials, direct labor, and factory overhead) are product costs. Nonmanufacturing overhead costs are the business expenses that are outside of a company’s manufacturing operations. In other words, these costs are not part of a manufacturer’s product cost or its production costs (which are direct materials, direct labor, and manufacturing overhead).

- These costs do not specifically contribute to the actual production of goods but are essential to ensure overall functioning of the business.

- Be sure to allocate overhead costs to the respective cost centers (specific departments, processes, or machines in the manufacturing facility that contribute to the manufacturing costs).

- These costs are reported on a company’s income statement below the cost of goods sold, and are usually charged to expense as incurred.

It is likely that you will have to estimate the cost of these activities. Next, you will need to allocate the cost of the activities to the individual products. Estimates and allocations based on logical assumptions are better than precise amounts based on faulty assumptions. For the past 52 years, Harold Averkamp (CPA, MBA) has worked as an accounting supervisor, manager, consultant, university instructor, and innovator in teaching accounting online. This article looks at meaning of and differences between two main cost categories for a manufacturing entity – manufacturing cost and non-manufacturing cost.

Since nonmanufacturing overhead costs are treated as period costs, they are not allocated to goods produced, as would be the case with factory overhead costs. Since they are not allocated to goods produced, these costs never appear in the cost of inventory on a firm’s balance sheet. Although selling costs and general and administrative costs are considered nonmanufacturing costs, managers often want to domestic partner assign some of these costs to products for decision-making purposes. For example, sales commissions and shipping costs for a specific product could be assigned to the product. However, as we noted earlier, managerial accounting information is tailored to meet the needs of the users and need not follow U.S. They form part of inventory and are charged against revenue, i.e. cost of sales, only when sold.

Note 1.43 “Business in Action 1.5” details the materials, labor, and manufacturing overhead at a company that has been producing boats since 1968. “When a manufacturer begins the production process, the costs incurred to create the products are initially recorded as assets in the form of WIP inventory. Manufacturing costs are recorded as assets (or inventory) in the company’s balance sheet until the finished goods are sold. As a result, the steel manufacturing company was able to achieve a 10% reduction in manufacturing costs and save €1 million (approximately $1.7 million) annually.

MasterCraft records these manufacturing costs as inventory on the balance sheet until the boats are sold, at which time the costs are transferred to cost of goods sold on the income statement. PepsiCo, Inc., produces more than 500 products under several different brand names, including Frito-Lay, Pepsi-Cola, Gatorade, Tropicana, and Quaker. Net sales for 2010 totaled $57,800,000,000, resulting in operating profits of $6,300,000,000. Cost of sales represented the highest cost on the income statement at $26,600,000,000. The second highest cost on the income statement—selling and general and administrative expenses—totaled $22,800,000,000. These expenses are period costs, meaning they must be expensed in the period in which they are incurred.

Material costs are the costs of raw materials used in manufacturing the product. Calculating manufacturing costs helps assess whether producing the product is going to be profitable for the company given the existing pricing strategy. By calculating manufacturing costs, manufacturers can better understand the elements that are driving up costs while identifying the most economical way to manufacture a product. Cost control, according to Fabrizi, is one of the top benefits of calculating manufacturing costs. Now, add the value of existing inventory to the cost of purchasing new inventory to calculate the cost of direct materials.